Innoviva’s Rollercoaster: Critical Care Bets With Respiratory Backing (NASDAQ:INVA)

")

Thomas Barwick

Introduction

Innoviva (NASDAQ:INVA) is a commercial-stage biopharma company focused on critical care and infectious disease therapeutics through its Innoviva Specialty Therapeutics division. The company also recognizes royalties from respiratory assets, like Relvar/Breo Ellipta and Anoro Ellipta, from a partnership with GSK plc (GSK). Lastly, Innoviva owns other strategic healthcare assets, such as a large equity stake in Armata Pharmaceuticals, a leader in development of bacteriophages with potential use across a range of infectious and other serious diseases. They also have “economic interests in other healthcare companies.” (Source)

Here are some upcoming catalysts for Innoviva:

|

Expected Date |

Catalyst | Details |

|---|---|---|

| Q4 2024 | NDA Submission for zoliflodacin | Innoviva is expected to submit a New Drug Application (NDA) for zoliflodacin, a potential first-in-class treatment for uncomplicated gonorrhea, following the completion of Phase 3 trials. |

| Early 2025 | Regulatory Decision for zoliflodacin | Pending the NDA submission, a regulatory decision is anticipated in early 2025. |

| Ongoing | Commercial Expansion of Xacduro | Following the approval of Xacduro in China, Innoviva plans to further expand its global footprint, with additional market launches and potentially increased sales in 2024-2025. |

| 2024-2025 | Updated Treatment Guidelines Impact | Continued recognition in key treatment guidelines for products like Xacduro and Xerava is expected to enhance market adoption and drive sales growth over the next year. |

| Ongoing | Partnership Developments | Innoviva continues to explore strategic partnerships and collaborations, particularly in expanding its critical care and infectious disease portfolio. |

Innoviva: High-Stakes Investments in a Shifting Biopharma Landscape

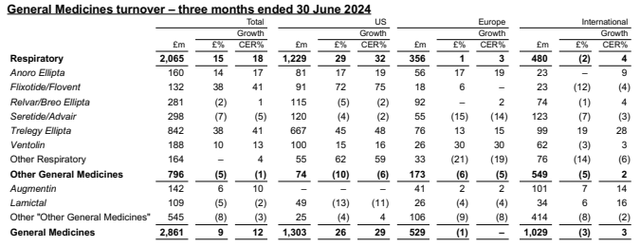

Relvar/Breo Ellipta (corticosteroid & β₂ agonist) and Anoro Ellipta (muscarinic antagonist & β2 agonist) are respiratory medications developed in collaboration by Innoviva and GSK. Both products are from the Ellipta inhaler line and are intended to treat chronic respiratory conditions. They were initially approved in 2013 for COPD. In 2022, a generic formulation of Breo Ellipta was released, resulting in a modest decline in sales for GSK. This decline is expected to accelerate within the next two years. It’s important to point out that GSK has no obligation to prioritize Breo Ellipta over, for example, their anticholinergic, corticosteroid, & β₂ agonist, Trelegy, which cannibalizes the former. Recall that in 2022 Innoviva sold all their equity interests in Theravance Respiratory Company, which was entitled to royalties on up to 10% of annual worldwide Trelegy sales. Trelegy, which is positioned as a more comprehensive treatment option, is far outperforming the others.

GSK Q2 Earnings

On the other hand, Anoro Ellipta has key patents expiring between 2025 and 2027. In Q2, GSK royalties totaled $67.2 million. GSK royalties have made up the majority of Innoviva’s revenues.

For Innoviva, this means the focus is shifting towards other products. What has the company done in the past decade to prepare?

In 2022, Innoviva made two key acquisitions by acquiring Entasis Therapeutics and La Jolla Pharmaceutical. The former cost approximately $113 million and added Xacduro (approved in 2023 for bacterial pneumonia). The latter cost $149 million and added Giapreza (approved in 2017 for septic shock) and Xerava (approved in 2018 for complicated intra-abdominal infections).

Together, they netted $21.7 million in Q2 2024 revenue for Innoviva.

| Product | Q2 2024 Sales |

|---|---|

| Giapreza | $13.1 million |

| Xerava | $6.2 million |

| Xacduro | $2.4 million |

| Total | $21.7 million |

Giapreza is one of several vasopressors and inotropes utilized to treat shock (hypotension). Having managed these intravenous “drips” myself, adrenergic agents like epinephrine and dopamine are almost without exception utilized first in this setting. Nonadrenergic agents like Giapreza (angiotensin II) are very seldom administered due to a lack of comparative efficacy with other vasopressor agents. As such, investors shouldn’t expect much growth from Giapreza.

Xerava is one of a few tetracyclines utilized for CRE intraabdominal infections. It is not a preferred agent. Judging from its Q2 sales performance following years on the market, investors shouldn’t expect much growth from Xerava unless there are favorable changes to treatment guidelines.

Finally, Xacduro, most recently approved in 2023, for the treatment of pneumonia caused by the acinetobacter baumannii-calcoaceticus complex, a difficult-to-treat form of pneumonia as a result of antibacterial resistance. However, Xacduro takes a seat to several available first-line options that are used extensively in clinical practice, such as cefepime and piperacillin-tazobactam. As such, investors shouldn’t expect much growth from Xacduro unless there are favorable changes to treatment guidelines.

Innoviva’s zoliflodacin is expected to hit the gonorrhea market next year but will face competition from standard-of-care treatments like ceftriaxone and azithromycin. In fact, a Phase 3 trial only proved zoliflodacin’s non-inferiority to this combination, despite lower cure rates for zoliflodacin compared to ceftriaxone and azithromycin (90.9% compared to 96.2%, respectively). The data has yet to be published in a reputable, peer-reviewed publication. However, its novel mechanism of action as a spiropyrimidinetrione antibiotic does set zoliflodacin apart, particularly against multidrug-resistant strains of gonorrhea. Given the relatively low cure rate and the lack of publication, zoliflodacin isn’t expected to be widely used in gonorrhea. As such, investors shouldn’t expect much from zoliflodacin unless there are favorable changes to treatment guidelines.

Financial Health

As of June 30, Innoviva reported $217 million in cash and cash equivalents. Total current assets were $358.277 million, while total current liabilities were just $28.206 million. Innoviva does owe $447.282 in “2025 and 2028 Convertible Senior Notes.”

In Q2, Innoviva reported a net loss of $34.685 million. This was mostly thanks to changes (expenses) in fair values of equity method investments totaling $90.66 million due to a “lower share price of Armata Pharmaceuticals.” Armata’s (ARMP) stock is down 23% in the past year.

While these are considered one-time expenses, ongoing declines in ARMP could continue to impact Innoviva’s finances. Innoviva has stakes in other companies as well.

In the first six months ending June 30, Innoviva brought in $80.765 million in cash from operating activities. Although I won’t estimate the cash runway, the company’s revenues are highly dependent on external factors such as ARMP stock price and GSK-related royalties. This dependence on external factors creates financial risk.

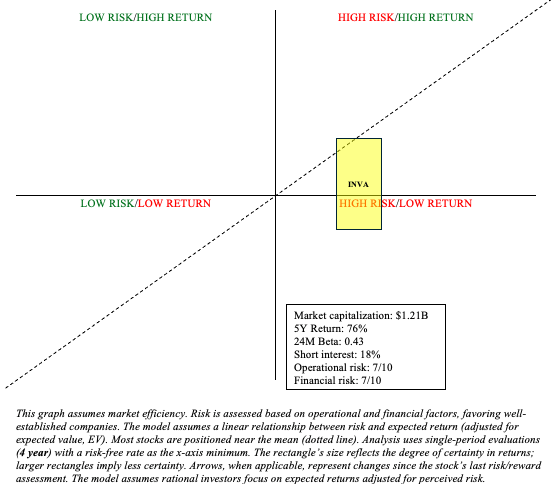

INVA Stock: Risk/Reward Assessment and Investment Recommendation

It goes without saying that Innoviva has many moving parts. So it is difficult to be certain about much when evaluating INVA stock for risk/reward. Its stock has rallied in the past year and trades near 52-week highs, but it’s hard to argue that INVA is overvalued. As Cantor recently pointed out after an overweight rating:

(…) it sees the company’s royalty stream from GSK respiratory products generating $1B+ over the next five years and its Innoviva Specialty Therapeutics, or IST, business achieving $1B+ in sales by 2033. Innoviva also has a portfolio of strategic investments in healthcare assets worth more than $600M.

On the flip side, it’s hard to really get excited about any particular prospect. I think it’s reasonable to believe that the royalty stream from GSK should diminish considerably within the next few years. I do not, however, share the same sentiment as Cantor in regard to their IST business. I do not see a path to $1B+ in sales by 2033 from the existing products. Cantor also cites the “portfolio of strategic investments in healthcare assets worth more than $600 million” as a positive, but this is also a risk and may continue to be negative (as evidenced by ARMP’s slumping stock).

Author

To conclude, INVA has mixed prospects. It is a Quadrant 1 investment (high risk/high return). It may work in a barbell portfolio. For my purposes, it’s a “hold” until their IST business has greater visibility. As always, investors are encouraged to maintain a diversified portfolio to mitigate idiosyncratic risks.

link